What manual reporting is truly costing organizations today

5 May 2026Every month, the same ritual repeats: gathering data, copying figures, manipulating Excel files, checking formulas… and only at the very end, when the deadline is already in sight, does the real work begin. Understanding what those figures actually mean.

For many finance teams, this is the reality. Manual reporting is so deeply embedded that it has become almost invisible. Spreadsheet reporting feels familiar, flexible, and controllable. But that is exactly where the danger lies. Because what seems manageable today is gradually growing into a structural blockade that undermines an organization's agility.

We see this across highly diverse organizations, from fast-growing SMEs to international groups. While the forms differ, the underlying dynamics in performance management are strikingly similar: fragmented financial operations, spreadsheet reporting, and legacy systems reinforce one another. Manual reporting is often viewed as a "free" alternative to process automation, BI tools, and system integrations. Despite all the advancements in automation in finance, many still revert to Excel because an "ad-hoc analysis" seems so quick to create, even when it becomes a recurring monthly task.

This costs your organization more than you might think...

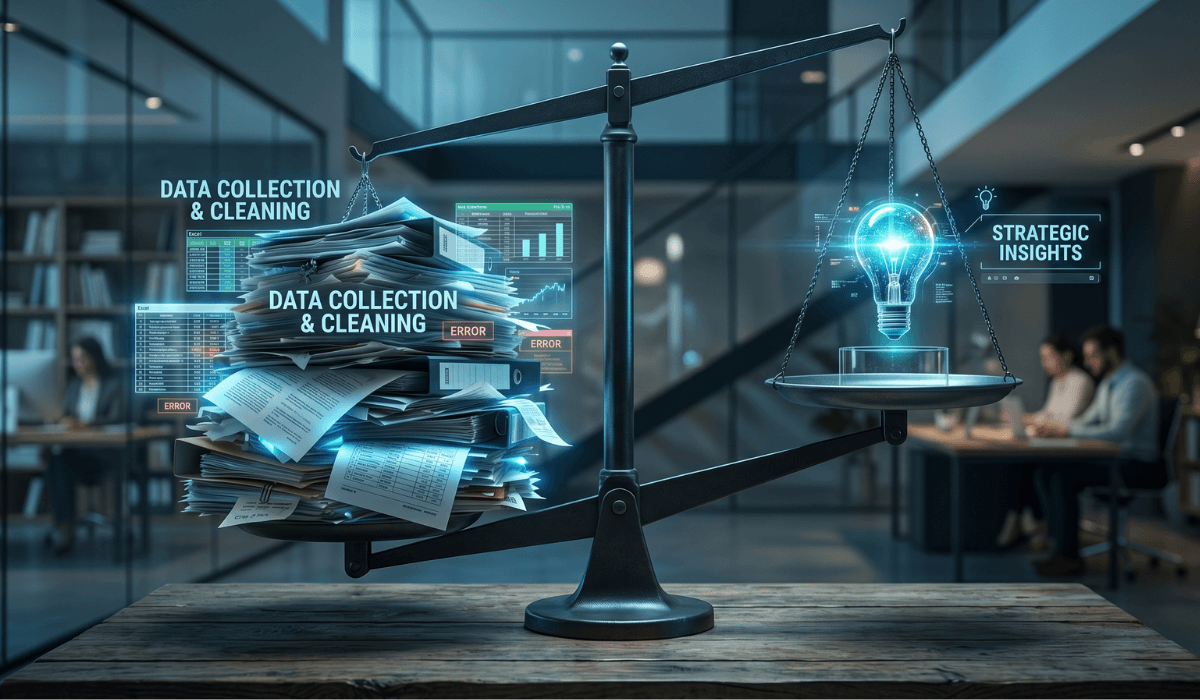

- Lack of scalability and continuity: Manual processes do not scale and create a snowball effect of operational inefficiency. The hidden costs in workload and frustration often only become painfully visible at critical breaking points, such as rapid growth or staff turnover.

- Governance as a foundation for steering: Data silos cause debates over the accuracy of figures rather than the necessary actions. Finance must evolve from a "report builder" to a "decision architect" through performance management that starts with the information needs of management.

- Strategic ROI and talent retention: Automation offers a higher return than manual processes by creating space for AI and forecasting. It increases retention; top talent prefers meaningful analysis over repetitive administration.

Manual reporting, even in automated environments

Why does manual reporting remain so dominant, even after significant investments in technology? The answer lies in accessibility. For many organizations, Excel feels like the ultimate freedom: it is flexible, quick to deploy, and everyone knows how to use it.

However, this flexibility has a dark side. As soon as an ad-hoc report becomes recurring, inefficiency creeps in. We regularly see companies that possess a Business Intelligence solution, yet still pour figures back into Excel to prepare them for presentations. This often indicates a lack of trust in system data or poor tool adoption within the organization.

Before you know it, a large part of your finance operations revolves around manual processes, risking a dangerous fragmentation of the truth.

Excel feels like the ultimate freedom for many organizations, but that freedom comes with a high price tag once an ad-hoc analysis becomes a recurring, inefficient routine.

Three weeks of gathering, one week of steering: the skewed balance of the month-end close

One of the most tangible costs of manual reporting is the enormous amount of time spent on non-value-adding tasks. In an efficient organization, finance acts as a strategic sparring partner; but in organizations stuck in spreadsheet reporting, the finance team functions more like a production unit.

Stuck in preparation: why 70% of time adds no value

We observe that many finance teams spend 60% to 70% of their time collecting, cleaning, and reconciling data. This leaves only 30% to 40% for actual analysis. The process of retrieving data from various sources, manually mapping dimensions, and correcting errors can take two to three weeks. By the time the figures are finally available, they are often already outdated.

Add a few days for creating a slide deck for management reporting, and there is hardly any time left for what really matters: analysis and sharing insights. Since the next closing cycle is always around the corner, process optimization becomes an afterthought. This is the vicious cycle of manual reporting.

The hidden labor cost of expertise

The question is not only how much time is lost, but also who is spending that time. It is not uncommon for chief accountants, finance managers, controllers, or FP&A analysts to spend hours retyping figures, reconciling data, and checking formulas. This represents an enormous waste of labor costs.

Furthermore, this manual pressure weighs heavily on the motivation and retention of finance professionals. Talented employees disengage when their job consists largely of 'patching holes' in flawed processes. Alternatively, they become overworked and face burnout. The hidden cost of this staff turnover, combined with the need to constantly train new people to execute manual and often poorly documented processes, constitutes a significant unrecorded expense.

Companies hire highly qualified finance experts for their analytical skills, yet let them work 70% of their time as data typists, patching holes in broken processes.

The snowball effect: the cost of manual processes compounds over the years

Manual reporting rarely becomes more efficient on its own as an organization grows. On the contrary, a snowball effect occurs where problems grow exponentially alongside the organization.

The accumulation of exceptions

In the beginning, an extra spreadsheet for a specific business unit remains manageable. However, over the years, more exceptions, ad-hoc solutions, and system silos are added. Every manual workaround originally created to compensate for a deficiency in the ERP system or accounting software becomes a permanent fixture of the monthly routine.

Growth through acquisitions

This effect becomes painfully clear when a growth strategy is based on acquisitions. If you acquire a company without reevaluating or automating its processes, you simply take on the entire manual workload of that new entity. Without automation in finance and a scalable reporting architecture, the organization will grind to a halt as soon as the complexity exceeds the employees’ individual capacity.

Lack of documentation and continuity

When processes are manual, knowledge often resides solely in the minds of individual employees and their ‘Excel magic’. During staff turnover, this knowledge is lost, leading to enormous risks for continuity. The company then runs the literal risk of stalling because no one knows exactly how that one crucial spreadsheet was built.

Legacy systems and the price of fragmentation

The root of manual reporting almost always lies in a fragmented system landscape and legacy software. Old legacy systems do not communicate with one another, causing data to become scattered across various silos.

Data silos and the battle for the truth

When sales reports from a sales module in an ERP or operational system and finance reports from the accounting records, two different versions of the truth inevitably emerge. There is no "single source of truth". Finance teams subsequently spend days reconciling these sources. The more systems involved, the higher the costs for these manual checks.

We often see that companies prefer "band-aid" fixes over a structural solution because they fear the significant investment required for an ERP update, financial reporting software, or a data warehouse. Organizations would rather spend money every month to rectify matters manually than release the budget at once to set it up correctly. Consequently, the hidden costs of staff turnover or delays in business operations remain under the radar.

The invisible impact on decision-making

The highest price an organization pays for manual reporting, however, is not found on the payroll, but manifests in the quality of decision-making. When the process of arriving at figures relies too heavily on human intervention, a dangerous dynamic emerges: finance shifts from a strategic sparring partner to a mere production unit, and crucial errors are made.

Analysis without added value

In a manual environment, there is often a lack of critical perspective on which analyses truly provide added value. Teams produce what is technically possible within existing systems, rather than fully committing to data-driven decision-making. This lack leads to:

- Discussions about the figure, not the action: As soon as there is a debate at the executive table about which figure is correct or which source it comes from, the reporting has failed.

- An excess of reports: What begins as a drive for transparency often ends in an overload of reports that no one actually uses anymore.

- Missed insights: The true hidden cost lies in the analyses that are not performed because the team is too busy cleaning data.

True data-driven decision making only arises when finance makes the transition from report builder to decision architect. This requires a management reporting format that does not start from the available data (supply-driven), but from the questions that management effectively needs to answer (demand-driven). Where data simplifies the conversation instead of slowing it down, the data-driven decision-making paradox disappears and room is created for genuine strategic value.

Errors with major consequences

Manual data integration and manual reporting in Excel are inherently prone to error. A formula that is not correctly dragged down or a manual adjustment in a spreadsheet can undermine the integrity of an entire report. Under intense time pressure, these errors often go unnoticed, leading to decisions based on incorrect data. The greatest risk is that a strategic path is taken based on a fundamentally flawed starting point.

This occurs more often than one would hope. Here are two examples from our professional experience:

- A significant inventory shortfall: A company with an EBITDA of three million euros had to take a half-million-euro hit to its P&L a few years after acquisition because the inventory valuation in the reporting did not match reality. The cause was the manual integration of data from an operational system and a separate, non-integrated accounting system. The consequences were significant: had the reporting at the time of acquisition shown correct data, the private equity player might have made a completely different decision.

- Flawed margin interpretation: A manufacturing company failed to correctly allocate transport costs from China to a specific product line of purchased goods, instead using a general allocation key to spread costs across its own manufactured products. This made the margin on imported products appear much larger than it actually was. This illustrates how manual and fragmented data allocation can lead to distorted margin insights and poses a real risk for incorrect strategic decisions.

A process error in a spreadsheet is an invisible risk that can remain unnoticed for years, until a 'reality check' exposes the actual financial damage.

Why the true cost often becomes visible too late

Why do organizations not intervene sooner? Because the costs of manual processes are often hidden in workload, frustration, and missed analyses. The impact is first felt by the people 'patching the holes', but they often lack the necessary levers to change the data and reporting architecture.

The true costs usually only become painfully clear at a critical breaking point:

- Strategic miscalculations: When policy choices rest on erroneous data, causing fundamental process errors to only surface once the financial damage has already been sustained.

- Growth: When the manual process is simply no longer scalable.

- Time pressure: When deadlines for banks or shareholders are no longer met.

- Staff turnover: When the only person who understood the reports leaves the organization.

Technology without structure only accelerates chaos. Governance is not a brake on progress, but the foundation to finally, truly navigate by the numbers.

The way forward: from report builder to decision architect

Breaking the cycle of manual reporting does not necessarily require more technology, but rather better foundations. We believe that finance plays a key role in this transition toward operational efficiency by bridging the gap between departments.

Building a uniform data platform

The first step is creating a central data platform (such as a data lakehouse or BI environment) where all data converges. This automates reconciliation and ensures a single version of the truth. It also immediately enables you to build control reports that instantly highlight errors in the source data.

Focus on decision relevance

Effective management reporting does not start from the data that happens to be available (supply-driven), but from the decisions that management actually needs to make (demand-driven). Limit the number of reports and pages to the essentials; focus creates decision-making power.

Governance is the prerequisite

Without clear agreements on definitions and ownership, any technological solution remains an empty shell. Establish who is responsible for which KPI and ensure that everyone speaks the same language. Data governance tools like dScribe can serve as the central foundation where all agreements regarding definitions and ownership come together in a single, clear, and shared source.

Streamlined reporting as a competitive advantage

Investing in the simplification and automation of reporting is not merely a cost item. It is an investment that delivers a competitive advantage in two crucial areas.

- Operational efficiency: When the finance team no longer has to spend days merely reconciling and compiling reports, time is freed up for genuine business partnering. That time is then used to perform rational checks on the figures and to make timely adjustments based on accurate reporting and forward-looking forecasts. In a world where data forms the basis for AI and advanced analytics, a central data platform is the only way to take that next step.

- Return on human capital and employee satisfaction: Business Intelligence and Business Analytics are domains that finance professionals are eager to delve into today. By investing in self-service tools, you offer them the opportunity to continuously develop themselves and help build the future of the organization. This not only lowers frustration on the work floor, but also limits the high costs of staff turnover often seen in departments with an excessive manual workload.

The budget spent on a modern reporting process ultimately yields a much higher return than the hidden costs caused by manual reporting.

Transition from manual reporting to a streamlined data and reporting architecture

Are you curious about where exactly the hidden costs in your current reporting process are located? We would be happy to help you sharpen the foundations of your financial management reporting. By making the switch from time-consuming manual actions to a smooth and streamlined process, finance transforms from a mere production unit into an efficient engine that supports the organization with timely and reliable insights. Where processes run smoothly and data simplifies the conversation instead of slowing it down, space finally emerges for true strategic value.